Alisa Gessler

Scientific Collaborator, HEC-UNIL

There is growing pressure on start-ups and SMEs to integrate ESG considerations into their governance and business activities. As of today, binding Swiss regulations on corporate sustainability disclosure and due diligence only target Swiss large companies. However, there are a number of benefits to implementing best practices, independently of company size. In an extremely complex and quickly evolving field, this guidance aims to provide a break-down for SMEs to better understand why keeping up with sustainability developments may be necessary for business opportunities in a shifting economy, and how to implement best practices relating to sustainability.

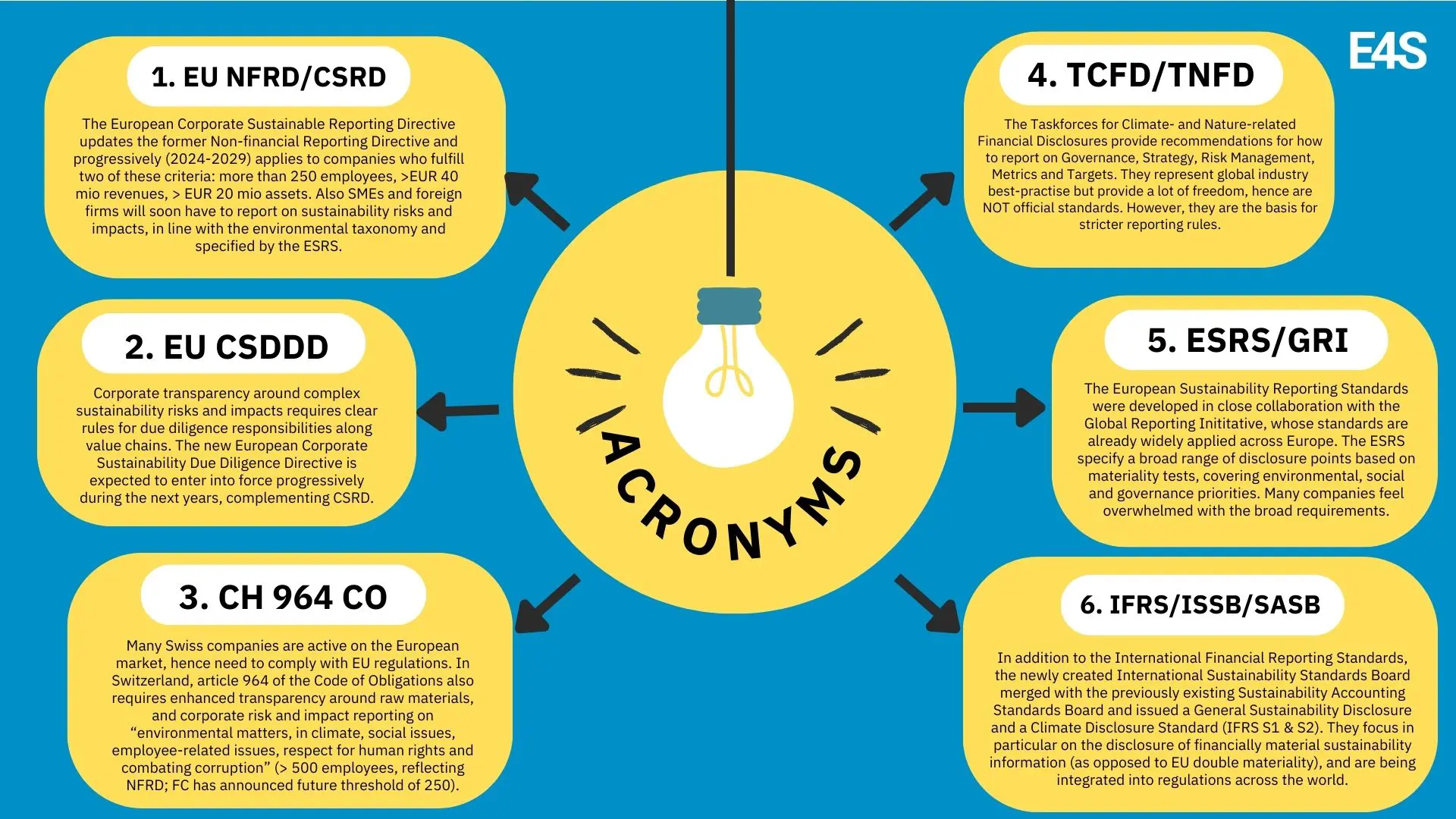

As of today, non-financial reporting is often the first step towards sustainable governance, as it occupies a predominant place among the contractual tools or legal measures aimed at improving the sustainability of a business. Therefore, we first explain the scope of novel Swiss, European and international reporting requirements and their impact on SMEs. We further highlight that the two main sets of sustainability reporting standards are both built around the recommendations of the global Taskforces on Climate- and Nature-related Disclosures (TCFD and TNFD). We recommend that SMEs familiarize themselves with those recommendations, thus prioritizing corporate sustainability information on Governance, Strategy, Risk Management and Metrics & Targets.

Secondly, moving from data gathering to action and impact, we highlight some of the tools and service providers that can help SMEs implement sustainability more generally in their management. In particular, we recommend some best-practice clauses, i.e. sustainability-oriented clauses that SMEs can include in their corporate documents to plant the seed for long-term corporate governance practices aligned with their strategy and commitments.

Disclaimer: We have taken all reasonable measures to ensure that the information presented in this document is complete, accurate, and up to date. However, this overview does not constitute legal advice and we disclaim all liability and responsibility towards persons or entities who use or consult this document.

It is reasonable to expect that international regulatory frameworks will evolve and, over time, lead to binding reporting norms for start-ups and SMEs. Non-EU countries such as the UK or Brazil have announced the regulatory incorporation of IFRS’ sustainability standards. In parallel, the European Sustainable Reporting Standards (ESRS) were finally adopted in October 2023.1 While these standards usually apply to large companies, their extension to smaller firms is discussed. In the EU, listed SMEs will be required to report sustainability-related information from the financial year 2026 (with the possibility of an additional two-year opt-out). Swiss start-ups and SMEs will be particularly impacted by these European requirements, because of the close economic ties with European countries.2

Meanwhile, the Swiss Federal Council has clarified its intentions to align national regulation with international developments. This includes the future expansion of the scope for compulsory sustainability reports to companies with more than 250 employees, and accepting EU reports and other OECD-aligned reports as equivalent.3 A trickle-down effect of reporting requirements is underway since these reporting obligations also require information on value chains. Against this backdrop, the Federal Council has been asked to draw up a report highlighting the possible direct and indirect effects of the new European and international ESG directives on Swiss SMEs.4 SMEs can uphold their competitive advantage by staying ahead of the game.

Investors and contractors are increasingly interested in companies that integrate ESG considerations into corporate governance. Swiss financial institutions and large corporations with branches or activities in Europe will increasingly request sustainability data from their supply chain partners, to fulfill their own due diligence obligations according to EU law. Some investors or large corporations already subject their investment or their contractual relationship to the fulfillment of a sustainability questionnaire, sustainability objectives, or other sustainability requirements. Not only can a company’s ESG integration be critical to the investment decision, but even filling out a sustainability questionnaire may require the collection of ESG data or the implementation of ESG processes. Some business partners contractually require ESG guarantees, e.g. in the form of a Code of Conduct, from their investees and suppliers to comply with their own ESG-related obligations.

Incorporating sustainable practices into an organization represents a proactive approach for businesses grappling with evolving legislation, shifts in natural resource availability, heightened customer expectations for sustainability, a growing demand for socially responsible employers, and a rising emphasis on ESG or sustainability criteria in investment decisions. The integration of sustainability into business practices serves as a strategic move, effectively future-proofing a business. This makes it a prudent choice for owners and managers committed to ensuring the longevity of their enterprise in the face of a dynamic and ever-changing global landscape.

To enhance sustainability, businesses should commence by comprehensively assessing their operational sustainability – a measure of how effectively they address environmental, social, and governance issues. Establishing a baseline is pivotal, as it forms the foundation for implementing targeted improvements over time. Various tools, including the Levo Framework, offer valuable resources for businesses seeking to undertake this transformative journey.

Shareholders and stakeholders more generally might expect and require that a firm adopts good governance practices relating to transparency, social engagement, ethical conduct, and so on. By integrating ESG considerations into corporate governance, a company shows its shareholders and stakeholders that sustainability matters and commits to taking these considerations seriously. Incorporating ESG considerations into corporate governance further helps to reduce companies’ risks and promotes the development of a positive corporate reputation. It contributes to building trust with shareholders and stakeholders more generally.

Incorporating sustainable practices into an organization represents a proactive approach for businesses grappling with evolving legislation, shifts in natural resource availability, heightened customer expectations for sustainability, a growing demand for socially responsible employers, and a rising emphasis on ESG or sustainability criteria in investment decisions. The integration of sustainability into business practices serves as a strategic move, effectively future-proofing a business. This makes it a prudent choice for owners and managers committed to ensuring the longevity of their enterprise in the face of a dynamic and ever-changing global landscape.

To enhance sustainability, businesses should commence by comprehensively assessing their operational sustainability – a measure of how effectively they address environmental, social, and governance issues. Establishing a baseline is pivotal, as it forms the foundation for implementing targeted improvements over time. Various tools, including the Levo Framework, offer valuable resources for businesses seeking to undertake this transformative journey.

Shareholders and stakeholders more generally might expect and require that a firm adopts good governance practices relating to transparency, social engagement, ethical conduct, and so on. By integrating ESG considerations into corporate governance, a company shows its shareholders and stakeholders that sustainability matters and commits to take these considerations seriously. Incorporating ESG considerations into the corporate governance further helps to reduce companies’ risks and promotes the development of a positive corporate reputation. It contributes to building trust with shareholders and stakeholders more generally.

Source: Enfinit/Pelt 8 2023

The TNFD is structured like the TCFD as it focuses on governance, strategy, risk management, and targets. It highlights not only nature risks to business but also non-financial business impacts on nature (so-called double materiality, see Figure above).6 Instead of shying away from the complexity of nature, it is crucial to keep in mind that climate change is only one driver of nature loss, in addition to invasive species, changes in land and sea use, pollution, and direct exploitation of natural resources. Taking climate change measures, without considering nature more holistically, can backfire. We suggest initially focusing on the natural aspects most interlinked with climate (e.g. forests and oceans as carbon sinks) and those closely associated with your business model.

Rather than thinking about impact measurement and sustainability reporting in terms of bureaucratic burden, firms should use the opportunity to reflect on business strategy and governance. Several public and private tools and initiatives exist to support companies in that endeavor. We further suggest simple legal phrases to include in a firm’s articles of association or shareholder agreement.

7) NERI-CASTRACANE ET AL., Legal Status for Sustainable Enterprise in Switzerland – White Paper from the Legal Experts Group, Alliance for Sustainable Enterprises, December 2023. https://www.alliance-sustainable- enterprises.ch/_files/ugd/fa1267_c073ec8c72a948af9c4995de67af6290.pdf

8) 23.454 | Introduire un statut juridique facultatif “Entreprise Durable” pour les PME suisses | Objet | Le Parlement suisse (parlament.ch)

9) https://www.parlament.ch/en/ratsbetrieb/suche-curia-vista/geschaeft?AffairId=20230454

An amendment to the Articles of Association may include a specific corporate purpose for your company and describe concrete actions the company is committed to. The corporate purpose (“raison d’être”) provides a framework for implementing the strategy and allocating resources in a consistent manner and inherently integrates the ESG components (BK-CHENAUX/BLANC, § 15 N 127).

In other words, shareholders can state in the Articles of Association how the company is to create sustainable value within the planetary boundaries while respecting the interests of its investors and other stakeholders (BK-CHENAUX/BLANC, § 15 N 127 s.).

This corporate purpose shall serve as a compass in the company’s risk policy and the directors’ decision process. It clarifies the board’s fiduciary duties about the company’s ESG objectives. The sustainability report may describe how the company implements this corporate purpose and the resources allocated (BK-CHENAUX/BLANC, § 15 N 155).

Purpose. The corporate purpose of the Company is to [insert as appropriate]. Through its business and operations, the Company shall strive for a material positive impact on society and environment.

Source of inspiration: Chancery Lane Project, Arlo’s Clause – ESG Aligned Company Articles (Link).

Purpose. The company’s objects are to carry on business as a general commercial company and, through its business and operations, to reduce or eliminate any process or activity within its control that releases GHGs and make every effort to achieve the goals of the Paris Agreement by implementing continuous, measured reductions in GHG emissions consistent with a maximum effort to achieve or exceed a fair share of the global 50% reduction in CO2 by 2030.

Source of inspiration: Chancery Lane Project, Pasfield’s Clause, Paris-Aligned Company Articles.

The Shareholders Agreement might describe the sustainability values and vision shared by the company’s owners, and detail the governance required to promote such values and support the vision.

Purpose. The Company, by pursuing its purpose, shall, through its business and operations, strive for a material positive impact on the society and the environment.

Company Values. The Shareholders acknowledge that the Company’s purpose and mission, as specified in the Articles of Association, shall be supported by (i) responsible business practices, (ii) the creation of short, mid and long term value for relevant stakeholders and (iii) a transition to sustainable economic activities in line with the United Nations’ Principles for Responsible Investment (collectively, the Company Values).

Sustainability. The Board shall manage the business of the Company in a manner which supports achieving the goals set forth in the UNFCCC Paris Agreement and the United Nations Sustainable Development Goals (2030 Agenda for Sustainable Development) (the Sustainability Goals).

Source: id est avocats

NB:

Non-Financial Reporting. The Board will regularly share with the Shareholders any non-

financial reporting information, such as ESG and climate related information, in line with the Mission, the Sustainability Goals or as imposed by the law, and will consider any reasonable requests by the Shareholders to expand such Non-Financial Reporting, in particular with a view to satisfy such Shareholders’ reporting and disclosure requirements.

Source: id est avocats

NB:

Annual Reporting. The Company shall further (i) produce an annual report with respect to its performance as evaluated against the ESG reporting framework it has adopted (the ESG Report) within 90 days after the end of each fiscal year of the Company following the adoption of the ESG reporting framework and (ii) comply with reasonable requests from its shareholders with respect to such shareholders’ ESG data collection efforts. The ESG Report shall include, at a minimum, (i) a description of the relevant objective targets and metrics; (ii) an objective assessment of the Company’s success in meeting such targets; and (iii) the Company’s proposed actions to further achieve the applicable targets over the next one-year period.

Source: id est avocats

Decision-making. In its decision-making process, the Board shall take into account the Company’s purpose, the short and long term interests of the Company, its subsidiaries and their suppliers, to create a positive material impact on society and the environment as well as the impact of their actions towards the relevant stakeholders, such as (i) their employees and their workforce, (ii) their customers, (iii) the regions and communities in which they are active and (iv) the environment.

Source: id est avocats

Decision-making. The Company shall procure that [major shareholders] (each, an Anchor Shareholder) be granted (i) a[n observer] seat at the Board[, and as such be invited to all Board meetings and receive all the information available to the Board] and (ii) an option, to be exercised at each Anchor Shareholder’s discretion, to assign to the Company or the other shareholders all of its shares in the Company, at the price originally paid by such Anchor Shareholder for such shares, in case the Company breaches any of its ESG obligations or covenants.

Furthermore, in the decision-making process, the Board shall give due consideration to ESG issues, even if such considerations may in some cases diverge from short-term financial gains. While maintaining the financial viability and interests of shareholders, the Board actively seeks opportunities to enhance the Company’s positive impact on the environment, society and governance practices, recognizing the importance of long-term sustainability and stakeholder value.

Source: id est avocats